Knowing the current inflation rate is helpful in making short term decisions. Seeing a table of historical inflation rates is only slightly productive. For long term planning, what we're really interested in is the annualized inflation over a period of time. Sure, some years inflation may skyrocket to 20%, but other years it's flat or even negative. Taken together, they should be equivalent to one inflation rate applied each year. This annualized inflation rate (or geometric mean, or Compound Annual Growth Rate [CAGR]) is probably a good value to use when modeling inflation far into the future.

I found some great information over at InflationData.com, but I couldn't find any information on average or annualized inflation. I found a calculator at MeasuringWorth.com, but that also wasn't terribly useful except to give me a single final result. Then I found Peter Dolph on average inflation, but that was unclear whether it gave an average year-over-year inflation, which didn't make as much intuitive sense, or the geometric mean. So, I decided to compute it myself.

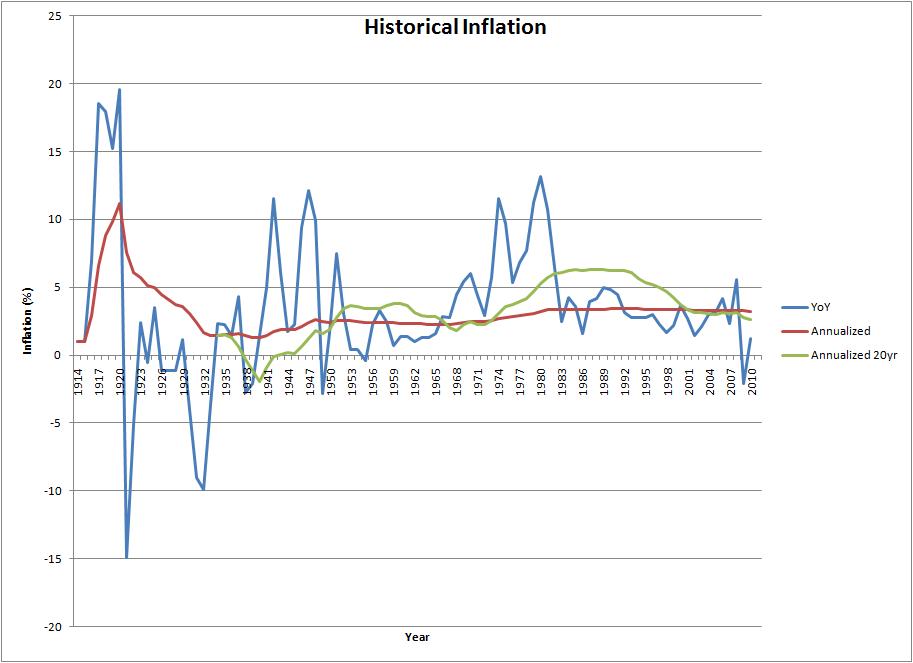

Since I love data, I started with the raw CPI data (see one of the tables below). I then computed the annualized inflation rate from 1913 up until each data point using the same month (or average, in the annual case) in each year. Looking at the table, things appeared to level out, so I decided to verify that with a graph! Not content with that, I then added the year-over-year inflation data for comparison purposes. Not content with that, I then computed and added a sliding 20-year window of annualized inflation rates.

The graph above (click for full size) shows the year-over-year inflation rate, a sliding 20-year annualized inflation rate, and an overall annualized inflation rate. Below, you can toggle between the raw CPI data and the overall annualized inflation rate table. The month of July was used for the graph for the simple reason that it was the most recent month data was available for this year. Also, the average 20-year annualized inflation rate was 3.236% compared to the overall annualized rate of 3.239% at the end of July, 2010, and compared to the 3.26% Peter Dolph found to be the average. Things seem to be pretty consistent.

"What about the risk of hyperinflation?" you may ask. Hyperinflation would indeed be bad, but I don't think it's particularly useful to worry about. If hyperinflation hits us, the world economy is likely completely broken and no amount of planning will help. You could argue that real goods like precious metals would hold their value, but I think owners of gold, for example, will have a hard time taking possession of that gold. Just a theory.

So, 3.3% is a pretty reasonable assumption for long term inflation, arrived at using various methods. This should give us some confidence when we create long term models and/or plans!

CPI Data Table Display Annualized Inflation Table| Year | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Annual |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 216.687 | 216.741 | 217.631 | 218.009 | 218.178 | 217.965 | 218.011 | --- | --- | --- | --- | --- | --- |

| 2009 | 211.143 | 212.193 | 212.709 | 213.240 | 213.856 | 215.693 | 215.351 | 215.834 | 215.969 | 216.177 | 216.330 | 215.949 | 214.537 |

| 2008 | 211.080 | 211.693 | 213.528 | 214.823 | 216.632 | 218.815 | 219.964 | 219.086 | 218.783 | 216.573 | 212.425 | 210.228 | 215.303 |

| 2007 | 202.416 | 203.499 | 205.352 | 206.686 | 207.949 | 208.352 | 208.299 | 207.917 | 208.490 | 208.936 | 210.177 | 210.036 | 207.342 |

| 2006 | 198.300 | 198.700 | 199.800 | 201.500 | 202.500 | 202.900 | 203.500 | 203.900 | 202.900 | 201.800 | 201.500 | 201.800 | 201.600 |

| 2005 | 190.700 | 191.800 | 193.300 | 194.600 | 194.400 | 194.500 | 195.400 | 196.400 | 198.800 | 199.200 | 197.600 | 196.800 | 195.300 |

| 2004 | 185.200 | 186.200 | 187.400 | 188.000 | 189.100 | 189.700 | 189.400 | 189.500 | 189.900 | 190.900 | 191.000 | 190.300 | 188.900 |

| 2003 | 181.700 | 183.100 | 184.200 | 183.800 | 183.500 | 183.700 | 183.900 | 184.600 | 185.200 | 185.000 | 184.500 | 184.300 | 183.960 |

| 2002 | 177.100 | 177.800 | 178.800 | 179.800 | 179.800 | 179.900 | 180.100 | 180.700 | 181.000 | 181.300 | 181.300 | 180.900 | 179.880 |

| 2001 | 175.100 | 175.800 | 176.200 | 176.900 | 177.700 | 178.000 | 177.500 | 177.500 | 178.300 | 177.700 | 177.400 | 176.700 | 177.100 |

| 2000 | 168.800 | 169.800 | 171.200 | 171.300 | 171.500 | 172.400 | 172.800 | 172.800 | 173.700 | 174.000 | 174.100 | 174.000 | 172.200 |

| 1999 | 164.300 | 164.500 | 165.000 | 166.200 | 166.200 | 166.200 | 166.700 | 167.100 | 167.900 | 168.200 | 168.300 | 168.300 | 166.600 |

| 1998 | 161.600 | 161.900 | 162.200 | 162.500 | 162.800 | 163.000 | 163.200 | 163.400 | 163.600 | 164.000 | 164.000 | 163.900 | 163.000 |

| 1997 | 159.100 | 159.600 | 160.000 | 160.200 | 160.100 | 160.300 | 160.500 | 160.800 | 161.200 | 161.600 | 161.500 | 161.300 | 160.500 |

| 1996 | 154.400 | 154.900 | 155.700 | 156.300 | 156.600 | 156.700 | 157.000 | 157.300 | 157.800 | 158.300 | 158.600 | 158.600 | 156.900 |

| 1995 | 150.300 | 150.900 | 151.400 | 151.900 | 152.200 | 152.500 | 152.500 | 152.900 | 153.200 | 153.700 | 153.600 | 153.500 | 152.400 |

| 1994 | 146.200 | 146.700 | 147.200 | 147.400 | 147.500 | 148.000 | 148.400 | 149.000 | 149.400 | 149.500 | 149.700 | 149.700 | 148.200 |

| 1993 | 142.600 | 143.100 | 143.600 | 144.000 | 144.200 | 144.400 | 144.400 | 144.800 | 145.100 | 145.700 | 145.800 | 145.800 | 144.500 |

| 1992 | 138.100 | 138.600 | 139.300 | 139.500 | 139.700 | 140.200 | 140.500 | 140.900 | 141.300 | 141.800 | 142.000 | 141.900 | 140.300 |

| 1991 | 134.600 | 134.800 | 135.000 | 135.200 | 135.600 | 136.000 | 136.200 | 136.600 | 137.200 | 137.400 | 137.800 | 137.900 | 136.200 |

| 1990 | 127.400 | 128.000 | 128.700 | 128.900 | 129.200 | 129.900 | 130.400 | 131.600 | 132.700 | 133.500 | 133.800 | 133.800 | 130.700 |

| 1989 | 121.100 | 121.600 | 122.300 | 123.100 | 123.800 | 124.100 | 124.400 | 124.600 | 125.000 | 125.600 | 125.900 | 126.100 | 124.000 |

| 1988 | 115.700 | 116.000 | 116.500 | 117.100 | 117.500 | 118.000 | 118.500 | 119.000 | 119.800 | 120.200 | 120.300 | 120.500 | 118.300 |

| 1987 | 111.200 | 111.600 | 112.100 | 112.700 | 113.100 | 113.500 | 113.800 | 114.400 | 115.000 | 115.300 | 115.400 | 115.400 | 113.600 |

| 1986 | 109.600 | 109.300 | 108.800 | 108.600 | 108.900 | 109.500 | 109.500 | 109.700 | 110.200 | 110.300 | 110.400 | 110.500 | 109.600 |

| 1985 | 105.500 | 106.000 | 106.400 | 106.900 | 107.300 | 107.600 | 107.800 | 108.000 | 108.300 | 108.700 | 109.000 | 109.300 | 107.600 |

| 1984 | 101.900 | 102.400 | 102.600 | 103.100 | 103.400 | 103.700 | 104.100 | 104.500 | 105.000 | 105.300 | 105.300 | 105.300 | 103.900 |

| 1983 | 97.800 | 97.900 | 97.900 | 98.600 | 99.200 | 99.500 | 99.900 | 100.200 | 100.700 | 101.000 | 101.200 | 101.300 | 99.600 |

| 1982 | 94.300 | 94.600 | 94.500 | 94.900 | 95.800 | 97.000 | 97.500 | 97.700 | 97.900 | 98.200 | 98.000 | 97.600 | 96.500 |

| 1981 | 87.000 | 87.900 | 88.500 | 89.100 | 89.800 | 90.600 | 91.600 | 92.300 | 93.200 | 93.400 | 93.700 | 94.000 | 90.900 |

| 1980 | 77.800 | 78.900 | 80.100 | 81.000 | 81.800 | 82.700 | 82.700 | 83.300 | 84.000 | 84.800 | 85.500 | 86.300 | 82.400 |

| 1979 | 68.300 | 69.100 | 69.800 | 70.600 | 71.500 | 72.300 | 73.100 | 73.800 | 74.600 | 75.200 | 75.900 | 76.700 | 72.600 |

| 1978 | 62.500 | 62.900 | 63.400 | 63.900 | 64.500 | 65.200 | 65.700 | 66.000 | 66.500 | 67.100 | 67.400 | 67.700 | 65.200 |

| 1977 | 58.500 | 59.100 | 59.500 | 60.000 | 60.300 | 60.700 | 61.000 | 61.200 | 61.400 | 61.600 | 61.900 | 62.100 | 60.600 |

| 1976 | 55.600 | 55.800 | 55.900 | 56.100 | 56.500 | 56.800 | 57.100 | 57.400 | 57.600 | 57.900 | 58.000 | 58.200 | 56.900 |

| 1975 | 52.100 | 52.500 | 52.700 | 52.900 | 53.200 | 53.600 | 54.200 | 54.300 | 54.600 | 54.900 | 55.300 | 55.500 | 53.800 |

| 1974 | 46.600 | 47.200 | 47.800 | 48.000 | 48.600 | 49.000 | 49.400 | 50.000 | 50.600 | 51.100 | 51.500 | 51.900 | 49.300 |

| 1973 | 42.600 | 42.900 | 43.300 | 43.600 | 43.900 | 44.200 | 44.300 | 45.100 | 45.200 | 45.600 | 45.900 | 46.200 | 44.400 |

| 1972 | 41.100 | 41.300 | 41.400 | 41.500 | 41.600 | 41.700 | 41.900 | 42.000 | 42.100 | 42.300 | 42.400 | 42.500 | 41.800 |

| 1971 | 39.800 | 39.900 | 40.000 | 40.100 | 40.300 | 40.600 | 40.700 | 40.800 | 40.800 | 40.900 | 40.900 | 41.100 | 40.500 |

| 1970 | 37.800 | 38.000 | 38.200 | 38.500 | 38.600 | 38.800 | 39.000 | 39.000 | 39.200 | 39.400 | 39.600 | 39.800 | 38.800 |

| 1969 | 35.600 | 35.800 | 36.100 | 36.300 | 36.400 | 36.600 | 36.800 | 37.000 | 37.100 | 37.300 | 37.500 | 37.700 | 36.700 |

| 1968 | 34.100 | 34.200 | 34.300 | 34.400 | 34.500 | 34.700 | 34.900 | 35.000 | 35.100 | 35.300 | 35.400 | 35.500 | 34.800 |

| 1967 | 32.900 | 32.900 | 33.000 | 33.100 | 33.200 | 33.300 | 33.400 | 33.500 | 33.600 | 33.700 | 33.800 | 33.900 | 33.400 |

| 1966 | 31.800 | 32.000 | 32.100 | 32.300 | 32.300 | 32.400 | 32.500 | 32.700 | 32.700 | 32.900 | 32.900 | 32.900 | 32.400 |

| 1965 | 31.200 | 31.200 | 31.300 | 31.400 | 31.400 | 31.600 | 31.600 | 31.600 | 31.600 | 31.700 | 31.700 | 31.800 | 31.500 |

| 1964 | 30.900 | 30.900 | 30.900 | 30.900 | 30.900 | 31.000 | 31.100 | 31.000 | 31.100 | 31.100 | 31.200 | 31.200 | 31.000 |

| 1963 | 30.400 | 30.400 | 30.500 | 30.500 | 30.500 | 30.600 | 30.700 | 30.700 | 30.700 | 30.800 | 30.800 | 30.900 | 30.600 |

| 1962 | 30.000 | 30.100 | 30.100 | 30.200 | 30.200 | 30.200 | 30.300 | 30.300 | 30.400 | 30.400 | 30.400 | 30.400 | 30.200 |

| 1961 | 29.800 | 29.800 | 29.800 | 29.800 | 29.800 | 29.800 | 30.000 | 29.900 | 30.000 | 30.000 | 30.000 | 30.000 | 29.900 |

| 1960 | 29.300 | 29.400 | 29.400 | 29.500 | 29.500 | 29.600 | 29.600 | 29.600 | 29.600 | 29.800 | 29.800 | 29.800 | 29.600 |

| 1959 | 29.000 | 28.900 | 28.900 | 29.000 | 29.000 | 29.100 | 29.200 | 29.200 | 29.300 | 29.400 | 29.400 | 29.400 | 29.100 |

| 1958 | 28.600 | 28.600 | 28.800 | 28.900 | 28.900 | 28.900 | 29.000 | 28.900 | 28.900 | 28.900 | 29.000 | 28.900 | 28.900 |

| 1957 | 27.600 | 27.700 | 27.800 | 27.900 | 28.000 | 28.100 | 28.300 | 28.300 | 28.300 | 28.300 | 28.400 | 28.400 | 28.100 |

| 1956 | 26.800 | 26.800 | 26.800 | 26.900 | 27.000 | 27.200 | 27.400 | 27.300 | 27.400 | 27.500 | 27.500 | 27.600 | 27.200 |

| 1955 | 26.700 | 26.700 | 26.700 | 26.700 | 26.700 | 26.700 | 26.800 | 26.800 | 26.900 | 26.900 | 26.900 | 26.800 | 26.800 |

| 1954 | 26.900 | 26.900 | 26.900 | 26.800 | 26.900 | 26.900 | 26.900 | 26.900 | 26.800 | 26.800 | 26.800 | 26.700 | 26.900 |

| 1953 | 26.600 | 26.500 | 26.600 | 26.600 | 26.700 | 26.800 | 26.800 | 26.900 | 26.900 | 27.000 | 26.900 | 26.900 | 26.700 |

| 1952 | 26.500 | 26.300 | 26.300 | 26.400 | 26.400 | 26.500 | 26.700 | 26.700 | 26.700 | 26.700 | 26.700 | 26.700 | 26.500 |

| 1951 | 25.400 | 25.700 | 25.800 | 25.800 | 25.900 | 25.900 | 25.900 | 25.900 | 26.100 | 26.200 | 26.400 | 26.500 | 26.000 |

| 1950 | 23.500 | 23.500 | 23.600 | 23.600 | 23.700 | 23.800 | 24.100 | 24.300 | 24.400 | 24.600 | 24.700 | 25.000 | 24.100 |

| 1949 | 24.000 | 23.800 | 23.800 | 23.900 | 23.800 | 23.900 | 23.700 | 23.800 | 23.900 | 23.700 | 23.800 | 23.600 | 23.800 |

| 1948 | 23.700 | 23.500 | 23.400 | 23.800 | 23.900 | 24.100 | 24.400 | 24.500 | 24.500 | 24.400 | 24.200 | 24.100 | 24.100 |

| 1947 | 21.500 | 21.500 | 21.900 | 21.900 | 21.900 | 22.000 | 22.200 | 22.500 | 23.000 | 23.000 | 23.100 | 23.400 | 22.300 |

| 1946 | 18.200 | 18.100 | 18.300 | 18.400 | 18.500 | 18.700 | 19.800 | 20.200 | 20.400 | 20.800 | 21.300 | 21.500 | 19.500 |

| 1945 | 17.800 | 17.800 | 17.800 | 17.800 | 17.900 | 18.100 | 18.100 | 18.100 | 18.100 | 18.100 | 18.100 | 18.200 | 18.000 |

| 1944 | 17.400 | 17.400 | 17.400 | 17.500 | 17.500 | 17.600 | 17.700 | 17.700 | 17.700 | 17.700 | 17.700 | 17.800 | 17.600 |

| 1943 | 16.900 | 16.900 | 17.200 | 17.400 | 17.500 | 17.500 | 17.400 | 17.300 | 17.400 | 17.400 | 17.400 | 17.400 | 17.300 |

| 1942 | 15.700 | 15.800 | 16.000 | 16.100 | 16.300 | 16.300 | 16.400 | 16.500 | 16.500 | 16.700 | 16.800 | 16.900 | 16.300 |

| 1941 | 14.100 | 14.100 | 14.200 | 14.300 | 14.400 | 14.700 | 14.700 | 14.900 | 15.100 | 15.300 | 15.400 | 15.500 | 14.700 |

| 1940 | 13.900 | 14.000 | 14.000 | 14.000 | 14.000 | 14.100 | 14.000 | 14.000 | 14.000 | 14.000 | 14.000 | 14.100 | 14.000 |

| 1939 | 14.000 | 13.900 | 13.900 | 13.800 | 13.800 | 13.800 | 13.800 | 13.800 | 14.100 | 14.000 | 14.000 | 14.000 | 13.900 |

| 1938 | 14.200 | 14.100 | 14.100 | 14.200 | 14.100 | 14.100 | 14.100 | 14.100 | 14.100 | 14.000 | 14.000 | 14.000 | 14.100 |

| 1937 | 14.100 | 14.100 | 14.200 | 14.300 | 14.400 | 14.400 | 14.500 | 14.500 | 14.600 | 14.600 | 14.500 | 14.400 | 14.400 |

| 1936 | 13.800 | 13.800 | 13.700 | 13.700 | 13.700 | 13.800 | 13.900 | 14.000 | 14.000 | 14.000 | 14.000 | 14.000 | 13.900 |

| 1935 | 13.600 | 13.700 | 13.700 | 13.800 | 13.800 | 13.700 | 13.700 | 13.700 | 13.700 | 13.700 | 13.800 | 13.800 | 13.700 |

| 1934 | 13.200 | 13.300 | 13.300 | 13.300 | 13.300 | 13.400 | 13.400 | 13.400 | 13.600 | 13.500 | 13.500 | 13.400 | 13.400 |

| 1933 | 12.900 | 12.700 | 12.600 | 12.600 | 12.600 | 12.700 | 13.100 | 13.200 | 13.200 | 13.200 | 13.200 | 13.200 | 13.000 |

| 1932 | 14.300 | 14.100 | 14.000 | 13.900 | 13.700 | 13.600 | 13.600 | 13.500 | 13.400 | 13.300 | 13.200 | 13.100 | 13.700 |

| 1931 | 15.900 | 15.700 | 15.600 | 15.500 | 15.300 | 15.100 | 15.100 | 15.100 | 15.000 | 14.900 | 14.700 | 14.600 | 15.200 |

| 1930 | 17.100 | 17.000 | 16.900 | 17.000 | 16.900 | 16.800 | 16.600 | 16.500 | 16.600 | 16.500 | 16.400 | 16.100 | 16.700 |

| 1929 | 17.100 | 17.100 | 17.000 | 16.900 | 17.000 | 17.100 | 17.300 | 17.300 | 17.300 | 17.300 | 17.300 | 17.200 | 17.100 |

| 1928 | 17.300 | 17.100 | 17.100 | 17.100 | 17.200 | 17.100 | 17.100 | 17.100 | 17.300 | 17.200 | 17.200 | 17.100 | 17.100 |

| 1927 | 17.500 | 17.400 | 17.300 | 17.300 | 17.400 | 17.600 | 17.300 | 17.200 | 17.300 | 17.400 | 17.300 | 17.300 | 17.400 |

| 1926 | 17.900 | 17.900 | 17.800 | 17.900 | 17.800 | 17.700 | 17.500 | 17.400 | 17.500 | 17.600 | 17.700 | 17.700 | 17.700 |

| 1925 | 17.300 | 17.200 | 17.300 | 17.200 | 17.300 | 17.500 | 17.700 | 17.700 | 17.700 | 17.700 | 18.000 | 17.900 | 17.500 |

| 1924 | 17.300 | 17.200 | 17.100 | 17.000 | 17.000 | 17.000 | 17.100 | 17.000 | 17.100 | 17.200 | 17.200 | 17.300 | 17.100 |

| 1923 | 16.800 | 16.800 | 16.800 | 16.900 | 16.900 | 17.000 | 17.200 | 17.100 | 17.200 | 17.300 | 17.300 | 17.300 | 17.100 |

| 1922 | 16.900 | 16.900 | 16.700 | 16.700 | 16.700 | 16.700 | 16.800 | 16.600 | 16.600 | 16.700 | 16.800 | 16.900 | 16.800 |

| 1921 | 19.000 | 18.400 | 18.300 | 18.100 | 17.700 | 17.600 | 17.700 | 17.700 | 17.500 | 17.500 | 17.400 | 17.300 | 17.900 |

| 1920 | 19.300 | 19.500 | 19.700 | 20.300 | 20.600 | 20.900 | 20.800 | 20.300 | 20.000 | 19.900 | 19.800 | 19.400 | 20.000 |

| 1919 | 16.500 | 16.200 | 16.400 | 16.700 | 16.900 | 16.900 | 17.400 | 17.700 | 17.800 | 18.100 | 18.500 | 18.900 | 17.300 |

| 1918 | 14.000 | 14.100 | 14.000 | 14.200 | 14.500 | 14.700 | 15.100 | 15.400 | 15.700 | 16.000 | 16.300 | 16.500 | 15.100 |

| 1917 | 11.700 | 12.000 | 12.000 | 12.600 | 12.800 | 13.000 | 12.800 | 13.000 | 13.300 | 13.500 | 13.500 | 13.700 | 12.800 |

| 1916 | 10.400 | 10.400 | 10.500 | 10.600 | 10.700 | 10.800 | 10.800 | 10.900 | 11.100 | 11.300 | 11.500 | 11.600 | 10.900 |

| 1915 | 10.100 | 10.000 | 9.900 | 10.000 | 10.100 | 10.100 | 10.100 | 10.100 | 10.100 | 10.200 | 10.300 | 10.300 | 10.100 |

| 1914 | 10.000 | 9.900 | 9.900 | 9.800 | 9.900 | 9.900 | 10.000 | 10.200 | 10.200 | 10.100 | 10.200 | 10.100 | 10.000 |

| 1913 | 9.800 | 9.800 | 9.800 | 9.800 | 9.700 | 9.800 | 9.900 | 9.900 | 10.000 | 10.000 | 10.100 | 10.000 | 9.900 |

| Year | Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sep | Oct | Nov | Dec | Annual |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2010 | 3.243 | 3.244 | 3.248 | 3.250 | 3.262 | 3.250 | 3.239 | --- | --- | --- | --- | --- | --- |

| 2009 | 3.250 | 3.255 | 3.258 | 3.260 | 3.275 | 3.273 | 3.260 | 3.262 | 3.252 | 3.253 | 3.243 | 3.252 | 3.256 |

| 2008 | 3.284 | 3.287 | 3.297 | 3.303 | 3.324 | 3.323 | 3.318 | 3.314 | 3.301 | 3.290 | 3.258 | 3.258 | 3.295 |

| 2007 | 3.274 | 3.280 | 3.289 | 3.297 | 3.315 | 3.305 | 3.294 | 3.292 | 3.284 | 3.286 | 3.282 | 3.292 | 3.289 |

| 2006 | 3.287 | 3.289 | 3.295 | 3.304 | 3.321 | 3.312 | 3.304 | 3.306 | 3.290 | 3.284 | 3.271 | 3.284 | 3.294 |

| 2005 | 3.279 | 3.286 | 3.294 | 3.302 | 3.312 | 3.301 | 3.295 | 3.301 | 3.303 | 3.305 | 3.285 | 3.292 | 3.294 |

| 2004 | 3.282 | 3.289 | 3.296 | 3.299 | 3.318 | 3.310 | 3.296 | 3.297 | 3.288 | 3.294 | 3.283 | 3.290 | 3.293 |

| 2003 | 3.298 | 3.306 | 3.313 | 3.311 | 3.321 | 3.310 | 3.300 | 3.304 | 3.296 | 3.295 | 3.281 | 3.291 | 3.300 |

| 2002 | 3.306 | 3.310 | 3.317 | 3.323 | 3.335 | 3.324 | 3.313 | 3.317 | 3.307 | 3.309 | 3.298 | 3.307 | 3.312 |

| 2001 | 3.330 | 3.335 | 3.338 | 3.342 | 3.360 | 3.350 | 3.334 | 3.334 | 3.328 | 3.324 | 3.310 | 3.317 | 3.332 |

| 2000 | 3.326 | 3.333 | 3.343 | 3.343 | 3.357 | 3.351 | 3.342 | 3.342 | 3.336 | 3.338 | 3.327 | 3.338 | 3.337 |

| 1999 | 3.333 | 3.334 | 3.338 | 3.346 | 3.359 | 3.346 | 3.338 | 3.341 | 3.334 | 3.337 | 3.325 | 3.337 | 3.337 |

| 1998 | 3.352 | 3.355 | 3.357 | 3.359 | 3.374 | 3.363 | 3.352 | 3.353 | 3.343 | 3.346 | 3.334 | 3.345 | 3.350 |

| 1997 | 3.374 | 3.378 | 3.381 | 3.382 | 3.394 | 3.383 | 3.372 | 3.374 | 3.365 | 3.368 | 3.355 | 3.366 | 3.372 |

| 1996 | 3.378 | 3.382 | 3.388 | 3.393 | 3.408 | 3.396 | 3.386 | 3.388 | 3.380 | 3.384 | 3.374 | 3.386 | 3.385 |

| 1995 | 3.386 | 3.391 | 3.395 | 3.399 | 3.414 | 3.404 | 3.391 | 3.394 | 3.384 | 3.388 | 3.375 | 3.387 | 3.390 |

| 1994 | 3.393 | 3.397 | 3.402 | 3.403 | 3.417 | 3.408 | 3.399 | 3.404 | 3.395 | 3.396 | 3.385 | 3.397 | 3.397 |

| 1993 | 3.404 | 3.408 | 3.413 | 3.416 | 3.431 | 3.420 | 3.407 | 3.410 | 3.400 | 3.405 | 3.393 | 3.406 | 3.408 |

| 1992 | 3.406 | 3.410 | 3.417 | 3.419 | 3.434 | 3.425 | 3.415 | 3.419 | 3.409 | 3.414 | 3.403 | 3.415 | 3.413 |

| 1991 | 3.416 | 3.418 | 3.420 | 3.422 | 3.439 | 3.430 | 3.418 | 3.422 | 3.415 | 3.416 | 3.407 | 3.421 | 3.418 |

| 1990 | 3.387 | 3.394 | 3.401 | 3.403 | 3.420 | 3.413 | 3.405 | 3.417 | 3.415 | 3.423 | 3.413 | 3.426 | 3.408 |

| 1989 | 3.364 | 3.369 | 3.377 | 3.386 | 3.407 | 3.397 | 3.386 | 3.388 | 3.379 | 3.386 | 3.375 | 3.391 | 3.382 |

| 1988 | 3.346 | 3.350 | 3.356 | 3.363 | 3.382 | 3.373 | 3.365 | 3.371 | 3.366 | 3.371 | 3.358 | 3.374 | 3.363 |

| 1987 | 3.337 | 3.342 | 3.348 | 3.356 | 3.375 | 3.365 | 3.355 | 3.362 | 3.356 | 3.359 | 3.346 | 3.360 | 3.352 |

| 1986 | 3.363 | 3.359 | 3.352 | 3.350 | 3.368 | 3.361 | 3.347 | 3.350 | 3.342 | 3.343 | 3.330 | 3.346 | 3.348 |

| 1985 | 3.356 | 3.362 | 3.368 | 3.374 | 3.395 | 3.384 | 3.372 | 3.375 | 3.364 | 3.369 | 3.359 | 3.377 | 3.369 |

| 1984 | 3.353 | 3.360 | 3.363 | 3.370 | 3.389 | 3.379 | 3.369 | 3.375 | 3.367 | 3.371 | 3.357 | 3.371 | 3.367 |

| 1983 | 3.341 | 3.343 | 3.343 | 3.353 | 3.377 | 3.367 | 3.357 | 3.362 | 3.354 | 3.359 | 3.347 | 3.363 | 3.353 |

| 1982 | 3.336 | 3.340 | 3.339 | 3.345 | 3.375 | 3.378 | 3.371 | 3.374 | 3.362 | 3.366 | 3.348 | 3.357 | 3.355 |

| 1981 | 3.263 | 3.279 | 3.289 | 3.299 | 3.327 | 3.325 | 3.326 | 3.338 | 3.337 | 3.340 | 3.330 | 3.350 | 3.314 |

| 1980 | 3.140 | 3.162 | 3.185 | 3.203 | 3.233 | 3.235 | 3.219 | 3.230 | 3.227 | 3.242 | 3.239 | 3.269 | 3.213 |

| 1979 | 2.985 | 3.004 | 3.019 | 3.037 | 3.073 | 3.074 | 3.076 | 3.090 | 3.092 | 3.104 | 3.103 | 3.135 | 3.065 |

| 1978 | 2.891 | 2.902 | 2.914 | 2.927 | 2.958 | 2.958 | 2.954 | 2.962 | 2.958 | 2.972 | 2.963 | 2.986 | 2.942 |

| 1977 | 2.831 | 2.847 | 2.858 | 2.872 | 2.896 | 2.890 | 2.882 | 2.887 | 2.876 | 2.881 | 2.873 | 2.894 | 2.871 |

| 1976 | 2.794 | 2.799 | 2.802 | 2.808 | 2.836 | 2.828 | 2.820 | 2.829 | 2.818 | 2.827 | 2.813 | 2.835 | 2.815 |

| 1975 | 2.731 | 2.744 | 2.750 | 2.757 | 2.783 | 2.778 | 2.780 | 2.783 | 2.776 | 2.785 | 2.780 | 2.803 | 2.768 |

| 1974 | 2.589 | 2.611 | 2.632 | 2.639 | 2.677 | 2.674 | 2.670 | 2.690 | 2.694 | 2.710 | 2.707 | 2.736 | 2.667 |

| 1973 | 2.479 | 2.491 | 2.507 | 2.519 | 2.548 | 2.542 | 2.529 | 2.559 | 2.546 | 2.561 | 2.555 | 2.583 | 2.533 |

| 1972 | 2.460 | 2.468 | 2.472 | 2.476 | 2.498 | 2.485 | 2.475 | 2.480 | 2.466 | 2.475 | 2.461 | 2.483 | 2.471 |

| 1971 | 2.446 | 2.450 | 2.455 | 2.459 | 2.486 | 2.481 | 2.467 | 2.472 | 2.454 | 2.458 | 2.441 | 2.467 | 2.459 |

| 1970 | 2.397 | 2.406 | 2.415 | 2.430 | 2.453 | 2.443 | 2.434 | 2.434 | 2.426 | 2.435 | 2.426 | 2.453 | 2.425 |

| 1969 | 2.330 | 2.340 | 2.356 | 2.366 | 2.390 | 2.381 | 2.372 | 2.382 | 2.369 | 2.379 | 2.370 | 2.398 | 2.367 |

| 1968 | 2.293 | 2.298 | 2.304 | 2.309 | 2.334 | 2.325 | 2.317 | 2.323 | 2.309 | 2.320 | 2.307 | 2.330 | 2.312 |

| 1967 | 2.268 | 2.268 | 2.274 | 2.280 | 2.305 | 2.291 | 2.277 | 2.283 | 2.270 | 2.275 | 2.262 | 2.287 | 2.277 |

| 1966 | 2.246 | 2.258 | 2.264 | 2.276 | 2.296 | 2.282 | 2.268 | 2.280 | 2.261 | 2.272 | 2.253 | 2.272 | 2.262 |

| 1965 | 2.252 | 2.252 | 2.258 | 2.265 | 2.285 | 2.277 | 2.257 | 2.257 | 2.237 | 2.244 | 2.224 | 2.250 | 2.251 |

| 1964 | 2.277 | 2.277 | 2.277 | 2.277 | 2.298 | 2.284 | 2.270 | 2.263 | 2.250 | 2.250 | 2.236 | 2.256 | 2.263 |

| 1963 | 2.290 | 2.290 | 2.297 | 2.297 | 2.318 | 2.303 | 2.289 | 2.289 | 2.269 | 2.275 | 2.255 | 2.282 | 2.283 |

| 1962 | 2.310 | 2.317 | 2.317 | 2.323 | 2.345 | 2.323 | 2.309 | 2.309 | 2.295 | 2.295 | 2.274 | 2.295 | 2.302 |

| 1961 | 2.344 | 2.344 | 2.344 | 2.344 | 2.366 | 2.344 | 2.337 | 2.329 | 2.315 | 2.315 | 2.294 | 2.315 | 2.329 |

| 1960 | 2.358 | 2.365 | 2.365 | 2.372 | 2.395 | 2.380 | 2.358 | 2.358 | 2.336 | 2.350 | 2.329 | 2.350 | 2.358 |

| 1959 | 2.387 | 2.379 | 2.379 | 2.387 | 2.409 | 2.394 | 2.379 | 2.379 | 2.364 | 2.372 | 2.350 | 2.372 | 2.372 |

| 1958 | 2.409 | 2.409 | 2.424 | 2.432 | 2.456 | 2.432 | 2.417 | 2.409 | 2.386 | 2.386 | 2.372 | 2.386 | 2.409 |

| 1957 | 2.381 | 2.390 | 2.398 | 2.406 | 2.439 | 2.423 | 2.416 | 2.416 | 2.392 | 2.392 | 2.377 | 2.401 | 2.399 |

| 1956 | 2.367 | 2.367 | 2.367 | 2.376 | 2.409 | 2.402 | 2.396 | 2.387 | 2.372 | 2.380 | 2.357 | 2.389 | 2.378 |

| 1955 | 2.415 | 2.415 | 2.415 | 2.415 | 2.440 | 2.415 | 2.399 | 2.399 | 2.384 | 2.384 | 2.360 | 2.375 | 2.399 |

| 1954 | 2.493 | 2.493 | 2.493 | 2.484 | 2.519 | 2.493 | 2.468 | 2.468 | 2.434 | 2.434 | 2.409 | 2.424 | 2.468 |

| 1953 | 2.528 | 2.518 | 2.528 | 2.528 | 2.564 | 2.547 | 2.521 | 2.530 | 2.505 | 2.514 | 2.479 | 2.505 | 2.511 |

| 1952 | 2.583 | 2.564 | 2.564 | 2.574 | 2.601 | 2.583 | 2.577 | 2.577 | 2.550 | 2.550 | 2.524 | 2.550 | 2.557 |

| 1951 | 2.538 | 2.570 | 2.580 | 2.580 | 2.618 | 2.591 | 2.563 | 2.563 | 2.557 | 2.567 | 2.561 | 2.598 | 2.574 |

| 1950 | 2.392 | 2.392 | 2.404 | 2.404 | 2.444 | 2.427 | 2.434 | 2.457 | 2.440 | 2.463 | 2.446 | 2.507 | 2.434 |

| 1949 | 2.519 | 2.495 | 2.495 | 2.507 | 2.525 | 2.507 | 2.454 | 2.466 | 2.450 | 2.426 | 2.410 | 2.414 | 2.466 |

| 1948 | 2.555 | 2.530 | 2.518 | 2.568 | 2.610 | 2.604 | 2.611 | 2.623 | 2.593 | 2.581 | 2.528 | 2.545 | 2.575 |

| 1947 | 2.338 | 2.338 | 2.393 | 2.393 | 2.424 | 2.407 | 2.404 | 2.444 | 2.480 | 2.480 | 2.463 | 2.532 | 2.417 |

| 1946 | 1.894 | 1.877 | 1.911 | 1.927 | 1.976 | 1.977 | 2.123 | 2.185 | 2.184 | 2.244 | 2.287 | 2.347 | 2.075 |

| 1945 | 1.883 | 1.883 | 1.883 | 1.883 | 1.933 | 1.936 | 1.903 | 1.903 | 1.871 | 1.871 | 1.840 | 1.889 | 1.886 |

| 1944 | 1.869 | 1.869 | 1.869 | 1.888 | 1.922 | 1.907 | 1.892 | 1.892 | 1.859 | 1.859 | 1.826 | 1.877 | 1.873 |

| 1943 | 1.833 | 1.833 | 1.893 | 1.932 | 1.986 | 1.952 | 1.898 | 1.878 | 1.863 | 1.863 | 1.830 | 1.863 | 1.878 |

| 1942 | 1.638 | 1.661 | 1.705 | 1.727 | 1.806 | 1.770 | 1.756 | 1.777 | 1.742 | 1.784 | 1.770 | 1.826 | 1.734 |

| 1941 | 1.308 | 1.308 | 1.333 | 1.359 | 1.421 | 1.459 | 1.422 | 1.471 | 1.483 | 1.530 | 1.518 | 1.578 | 1.422 |

| 1940 | 1.303 | 1.330 | 1.330 | 1.330 | 1.368 | 1.356 | 1.292 | 1.292 | 1.254 | 1.254 | 1.217 | 1.281 | 1.292 |

| 1939 | 1.381 | 1.353 | 1.353 | 1.325 | 1.365 | 1.325 | 1.286 | 1.286 | 1.330 | 1.303 | 1.264 | 1.303 | 1.314 |

| 1938 | 1.494 | 1.466 | 1.466 | 1.494 | 1.507 | 1.466 | 1.425 | 1.425 | 1.384 | 1.355 | 1.315 | 1.355 | 1.425 |

| 1937 | 1.527 | 1.527 | 1.557 | 1.587 | 1.660 | 1.616 | 1.603 | 1.603 | 1.589 | 1.589 | 1.518 | 1.531 | 1.573 |

| 1936 | 1.499 | 1.499 | 1.467 | 1.467 | 1.512 | 1.499 | 1.486 | 1.518 | 1.474 | 1.474 | 1.430 | 1.474 | 1.486 |

| 1935 | 1.501 | 1.534 | 1.534 | 1.568 | 1.615 | 1.534 | 1.488 | 1.488 | 1.441 | 1.441 | 1.429 | 1.475 | 1.488 |

| 1934 | 1.428 | 1.465 | 1.465 | 1.465 | 1.514 | 1.501 | 1.452 | 1.452 | 1.475 | 1.439 | 1.391 | 1.403 | 1.452 |

| 1933 | 1.384 | 1.305 | 1.265 | 1.265 | 1.316 | 1.305 | 1.410 | 1.449 | 1.398 | 1.398 | 1.347 | 1.398 | 1.371 |

| 1932 | 2.009 | 1.933 | 1.895 | 1.857 | 1.834 | 1.740 | 1.685 | 1.646 | 1.552 | 1.512 | 1.419 | 1.431 | 1.724 |

| 1931 | 2.725 | 2.653 | 2.616 | 2.580 | 2.564 | 2.431 | 2.373 | 2.373 | 2.278 | 2.240 | 2.107 | 2.125 | 2.411 |

| 1930 | 3.329 | 3.293 | 3.257 | 3.293 | 3.320 | 3.221 | 3.087 | 3.050 | 3.026 | 2.990 | 2.892 | 2.841 | 3.124 |

| 1929 | 3.541 | 3.541 | 3.503 | 3.464 | 3.569 | 3.541 | 3.550 | 3.550 | 3.485 | 3.485 | 3.421 | 3.448 | 3.475 |

| 1928 | 3.862 | 3.781 | 3.781 | 3.781 | 3.892 | 3.781 | 3.711 | 3.711 | 3.722 | 3.682 | 3.613 | 3.641 | 3.711 |

| 1927 | 4.229 | 4.186 | 4.143 | 4.143 | 4.262 | 4.271 | 4.067 | 4.024 | 3.993 | 4.036 | 3.919 | 3.993 | 4.110 |

| 1926 | 4.743 | 4.743 | 4.698 | 4.743 | 4.781 | 4.653 | 4.479 | 4.433 | 4.399 | 4.445 | 4.410 | 4.490 | 4.571 |

| 1925 | 4.850 | 4.799 | 4.850 | 4.799 | 4.940 | 4.950 | 4.961 | 4.961 | 4.873 | 4.873 | 4.933 | 4.971 | 4.862 |

| 1924 | 5.302 | 5.247 | 5.191 | 5.135 | 5.233 | 5.135 | 5.094 | 5.038 | 4.998 | 5.054 | 4.959 | 5.109 | 5.094 |

| 1923 | 5.538 | 5.538 | 5.538 | 5.601 | 5.709 | 5.663 | 5.679 | 5.618 | 5.573 | 5.634 | 5.529 | 5.634 | 5.618 |

| 1922 | 6.242 | 6.242 | 6.101 | 6.101 | 6.222 | 6.101 | 6.052 | 5.911 | 5.793 | 5.864 | 5.817 | 6.004 | 6.052 |

| 1921 | 8.628 | 8.193 | 8.119 | 7.971 | 7.808 | 7.593 | 7.533 | 7.533 | 7.246 | 7.246 | 7.036 | 7.092 | 7.684 |

| 1920 | 10.166 | 10.328 | 10.489 | 10.964 | 11.360 | 11.427 | 11.189 | 10.803 | 10.409 | 10.330 | 10.094 | 9.930 | 10.568 |

| 1919 | 9.071 | 8.738 | 8.961 | 9.290 | 9.695 | 9.507 | 9.855 | 10.168 | 10.087 | 10.394 | 10.614 | 11.193 | 9.749 |

| 1918 | 7.394 | 7.547 | 7.394 | 7.699 | 8.373 | 8.447 | 8.810 | 9.239 | 9.441 | 9.856 | 10.046 | 10.534 | 8.810 |

| 1917 | 4.530 | 5.193 | 5.193 | 6.484 | 7.179 | 7.320 | 6.634 | 7.048 | 7.390 | 7.791 | 7.523 | 8.188 | 6.634 |

| 1916 | 2.001 | 2.001 | 2.326 | 2.650 | 3.325 | 3.292 | 2.943 | 3.260 | 3.540 | 4.158 | 4.422 | 5.072 | 3.260 |

| 1915 | 1.519 | 1.015 | 0.509 | 1.015 | 2.041 | 1.519 | 1.005 | 1.005 | 0.499 | 0.995 | 0.985 | 1.489 | 1.005 |

| 1914 | 2.041 | 1.020 | 1.020 | 0.000 | 2.062 | 1.020 | 1.010 | 3.030 | 2.000 | 1.000 | 0.990 | 1.000 | 1.010 |

| 1913 | --- | --- | --- | --- | --- | --- | --- | --- | --- | --- | --- | --- | --- |

2 comments:

As an economist, I must object to one little tidbit: "real goods like precious metals". Gold, silver, et al. are just as arbitrary as fiat money; their "real" value is quite low (aside from the very tiny amounts used in electronics and frivolous vanity, what exactly is the intrinsic utility of gold?). And if there is an economic meltdown and collapse into autarky so severe that it knocks the USD into hyperinflation, then in all likelihood, gold or silver would be just as worthless.

// KL

Thanks for commenting! I haven't looked into it in detail, but one thing the proponents of gold keep pointing to is how X amount of gold has been equal to Y amount of gas for Z number of years (or maybe they're picking the two years they use as examples very carefully). I'm not a proponent of gold in any way, really. Partially for the reason you mention, and partially for the reason I mention (I don't think owning it will do you any good in a crisis), and partially because I'm not convinced it's a better inflation hedge than the stock market.

I think metals are slightly less arbitrary than paper money, however. You can easily print more money, but it takes actual effort to mine more metal. It doesn't particularly matter what is used as long as there is confidence in the currency, and there has historically been confidence in gold, even in inflationary times. That's not to say metals are ideal, or that their current value is deserved in any way. I think the price of gold is a better indicator of global fear levels than anything. ;)

Post a Comment